Choosing a legal structure for your business is a little bit like choosing your character in a video game: you usually have a few to choose from, and each has its strengths and weaknesses depending on the situation. Your legal structure is a very important aspect of your business—it will impact almost every decision you make, from who you go into business with to how you find funding. Taking time to understand the business structures available to you and choosing the correct one can save you thousands of dollars per year, and ultimately decide whether your business succeeds or fails.

There are several business entity types to choose from, each with varying levels of personal liability, tax obligations, ownership rules, and administrative complexity. We’ve made it as simple as possible for online merchants to choose the right option for their business.

In this guide, we’ll cover:

- A breakdown of each type of business structure

- How to choose the right structure for your business

Breakdown of Business Structures for Online Merchants

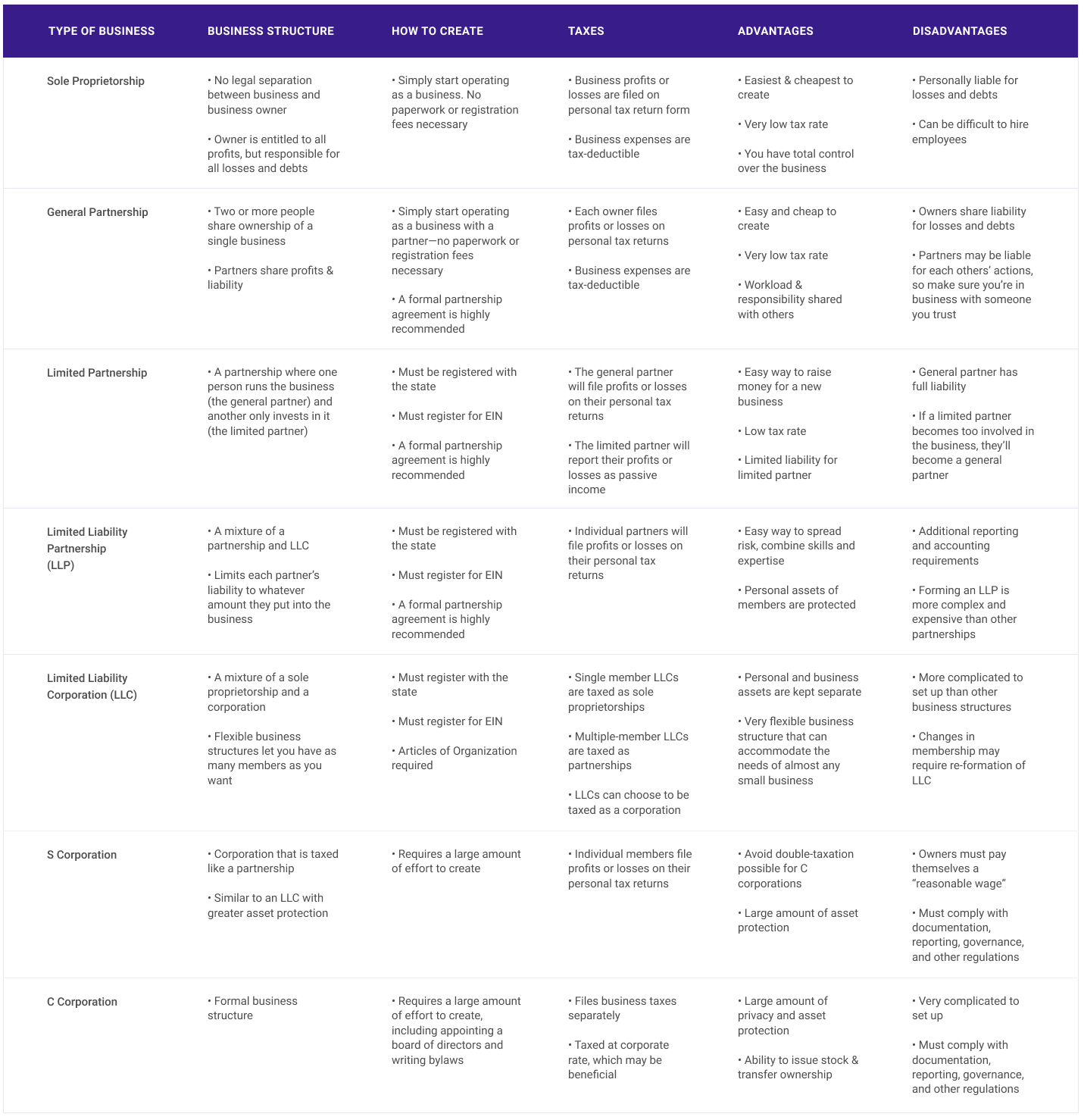

The IRS (internal revenue service) formally recognizes dozens of types of business entities, but only a few are relevant for online merchants. Let’s review the most common types of business structures for online merchants, along with perks and disadvantages of each.

Most Popular for Online Merchants: Sole Proprietorship

As the name implies, this type of business entity is owned and operated by a single person. The main benefit of a sole proprietorship is that it requires almost no paperwork to get started—you form the business simply by operating as the business. This structure is most popular for dropshippers and print-on-demand merchants, small owned-and-operated hobby businesses, and people who want to keep their taxes as simple as possible. If you just want to get started in ecommerce without needing to do a lot of paperwork or complicating your taxes, a sole proprietorship is right for you.

Paperwork needed

Almost none. No forms are required to create the business at the state or federal level, although the business may be required to get local permits to operate legally. The permits you need vary from city to city, so check your local Small Business Administration (SBA) website or with your local city hall.

Tax obligation

Profit-dependant. Personal taxes based on your income bracket and self-employment tax (15.9% as of 2019) are assessed each year. For ecommerce merchants, taxes on sole proprietorships tend to be lower than other businesses.

Registration cost

None—simply by operating as a business, you have formed a sole proprietorship. You are not required to fill out any forms or pay any registration fees. You also are not required to register your business as a tax entity since you’ll be paying taxes on your own personal tax return.

Liability

Very high. 100% of personal assets (car, home, etc.) are linked to the retail brand. If you incur debts in your business’ name, creditors can sue you personally to collect the debt. Conversely, if you have personal debts that are unpaid, creditors can go after your business profits to satisfy the debt. Since a Sole Proprietorship doesn’t exist as a separate legal entity, owners must conduct all business in their personal name, meaning that the owner is personally responsible for all business dealings.

Most ecommerce merchants find this level of liability to be acceptable. Just be aware that you’ll be personally liable for anything you buy in your business’ name, so be responsible when making purchases or signing contracts.

Benefits

- Lowest barrier to entry—you form the business simply by acting as a business

- No application or forms to fill out

- Simple and quick to start or dissolve; good for starting out or testing an idea

- Inexpensive, with no application costs

- Retain single-person control over all business decisions

- All profits are your own

- Startup costs are tax-deductible

Drawbacks

- No legal distinction between you and your business

- Can be tricky to expand or hire new employees

- You won’t be able to open business bank accounts or build business credit

- 100% liability for accrued debts and financial losses

- No personal protections for lawsuits filed against your business

- Owner pays self-employment and income taxes based on business earnings

- Taxes are sometimes higher than corporate rates

Best for

- People who are owning and operating their business alone

- Entrepreneurs who are planning to operate a structurally-simple business (like an online store)

- Businesses with little startup capital

- People who don’t want to file separate business taxes

- Testing business ideas or getting a toehold in a market

If you want to operate your business as yourself and avoid as many hassles associated with starting a business as possible, then a Sole Proprietorship is the best business structure for you. While operating this type of business saves time and money, keep in mind that you must personally take responsibility for all costs and issues associated with the business.

Best for Two- or Three-Person Startups: Partnerships

If you’re starting a business with one or more partners, you may want to choose to form a partnership. Partnerships are flexible because they allow members to assign different levels of responsibility and liability amongst themselves. Partnerships work best for joint ventures with two or more members sharing responsibility for the business, or for businesses receiving funding from an investor. There are three main types of partnerships:

- A General Partnership (GP) is very easy to form, requiring no paperwork—simply by going into business with another person, you’ve formed a general partnership. It’s similar to forming a Sole Proprietor, but with partner(s).

- A Limited Partnership (LP) lets one person (known as the “general partner”) operate the day-to-day operations of a business while the other invests without taking an active role in the business (known as a “silent partner”).

- A Limited Liability Partnership (LLP) is a mixture of a limited liability company (LLC) and a partnership. All partners have a say in how the business is operated, and the amount of personal liability of all partners is reduced. The amount of liability protection offered by a Limited Liability Partnership varies by state.

Paperwork

- General Partnership: Almost none. GPs require no paperwork or registration to begin. By acting as a business, you and your partner have formed a general partnership. You may still need to get local permits in order to operate legally—check your local SBA or City Hall. It’s also highly recommended that ALL partnerships create and sign a formal partnership agreement detailing the responsibilities of each member.

- Limited Partnership: Low. In most states, you must file for a Certificate of Limited Partnership, but the paperwork required tends to be low. As with all businesses, you might need to apply for local permits. It’s also highly recommended that you create a formal partnership agreement.

- Limited Liability Partnership (LLP): Medium. You’ll need to file for a certificate of limited liability partnership, file for local permits, and register for an EIN for your business. While the full requirements vary by state, the cost for forming an LLP is usually between $300-500, and filling out the paperwork can usually be done in one afternoon.

Tax obligation

Profit-dependant. Personal taxes based on your income bracket and self-employment tax (15.9% as of 2019) are assessed each year. GPs and LPs will pay taxes on individual members’ personal tax returns, while LLPs will pay business taxes separately.

Registration costs

None for a GPs. LP and LLP registration fees vary by state, but are typically around $300-500.

Liability

GPs and LPs both have high levels of liability. Like Sole Proprietorships, there is no separation between the business and its owners, so owners will be personally liable for any debts or obligations accrued in the business’ name.

LLPs limit the level of personal liability for members, as the name implies. While the level of liability protection varies by state, members of an LLP will always have lower levels of personal liability for the business than in other types of partnerships.

Benefits

- General Partnership is very easy to start—no paperwork or registration required

- Multiple levels of liability protection to choose from

- Tend to be inexpensive and simple to start

- Can pool resources and talent with others

- Can choose whether to pay taxes on personal returns or as a separate business entity

Drawbacks

- You can be liable for the actions of your partner(s)

- The partnership can dissolve if a member quits

- Partners must agree on business decisions

- LLPs are not available to ecommerce merchants in some states

- Can be difficult to remove or replace a partner

Best for

- Groups of 2-3 individuals going into business with one another

- Businesses funded by private investors

- Those who prefer a simplified business structures and taxes

Partnerships allow you to go into business with those you know and trust well, and are useful for those wishing to pool talent or financial resources. Even if you know and trust your partner well, it’s recommended that every partnership creates a partnership agreement to clearly delineate individual responsibilities, liabilities, and set the rules by which the partnership will operate.

Best for Serious Startups: Limited Liability Company (LLC)

While setting up an LLC isn’t terribly difficult, it takes more time and paperwork than a Sole Proprietorship or General Partnership. In exchange, it offers members insulation between their personal and business affairs.

For business owners who want to maintain control over their brand while keeping their business’ retail assets and personal assets separate, an LLC is a popular form of incorporation. It’s like a mixture between a corporation and a partnership, letting business owners maintain large amounts of control over business decisions while enjoying protection from personal liability. However, there’s far less regulation than a formal corporation, and the process of incorporating isn’t much more extensive than forming a formal business partnership.

Paperwork needed

Moderate. Requires at least: Name Search and New Business Registration, Articles of Organization, Operating Agreement, and Business Licenses.

Tax obligation

Owner’s choice. Can choose to pay taxes on individual tax returns (pass-through taxation) or be taxed as a corporation.

Registration cost

Moderate. Registration costs vary by state but are typically between $300-500.

Liability

Low. Owners and business assets are considered separate.

Benefits

- Lower personal liability for partners

- Unlimited number of partners allowed

- Less paperwork and administrative operations than a corporation

- Flexible flow-through taxation of your choice

- Profits aren't double-taxed

- Tax write-offs and profits are not dependent on ownership percentages

- You own the rights to your business name

- Credibility with customers

Drawbacks

- Must maintain business records and financial statements

- No stock options

- Formal annual meetings usually required

- Annual renewal and compliance fees may apply

- More difficult to raise business capital than under an LP

- LLC must be dissolved and re-established when any member leaves

- Tax rates increase with profits

Best for

- People who want to legally separate their business and personal affairs

- People looking for a simple, adaptable business structure that doesn’t require tons of paperwork

- People wanting the credibility and stability associated with the corporate business model

- Businesses planning to stay small- to medium-sized

LLCs let you form a more formal, legitimate business without having to do mountains of paperwork. They allow you to go into business with others, choose a tax structure that benefits you, and provide a high level of protection from personal liability—in other words, they give you most of the benefits of forming a corporation while being much simpler and easier to set up. Additionally, having an LLC will provide your business with a greater level of authority and respectability in the eyes of your customers.

Best for Large Businesses: Corporation

Though it’s rare, some ecommerce merchants choose to establish themselves as a formal, fully-independent corporation, even if it does mean strict operating and reporting obligations. This keeps them protected from any personal liability by making it a totally separate entity in the eyes of the IRS.

Paperwork needed

High. Corporations involve extensive paperwork and complex legal requirements including name selection and clearance, assembling a board of directors, filing articles of incorporation, creating corporate by-laws, annual board meetings, issuing shareholder stock certificates, and more. You’ll likely need to hire a lawyer and accountant to help you set everything up correctly.

Tax obligation

High. Corporate taxes were assessed at 21% as of 2019, plus personal taxes are paid based on your wages or dividend shares.

Registration cost

High. Costs exceed several hundred dollars for the initial registration plus annual renewal fees that vary depending on your state.

Liability

None. Business losses, debts, and settlements are all distinct from personal assets.

Benefits

- Complete liability protection for owners and shareholders

- Personal asset protection from creditors

- Profit retention without owner tax

- Ability to raise capital and create stock options

- Can persist when owners or partners quit or pass away

Drawbacks

- Expensive and complicated to file and maintain

- Higher tax rates than other business structures

- Double taxation for business and personal income

- Heavy operating and reporting regulation with no flexibility

- Usually requires attorney fees to get set up properly

Best for

- Large, formal business ventures

- Businesses planning on hiring employees or expanding into multiple locations

- Businesses seeking to raise capital

If you’ve got some capital to help start your business or already have employees, you may want to consider a corporation. Corporations are highly complex to start and maintain, but make up for this with some significant business benefits: you can raise capital as you choose, expand franchises between states or internationally, and hire employees as necessary.

Alternate Option: S Corporation

Looking to keep your business under 100 people? You could get the same asset protection as a corporation, but pay taxes like a partnership if you qualify as an S Corporation (S Corp). Your operating procedures will still be inflexible, but you’ll retain some limited stock options and avoid the corporate tax rate. S Corps can also claim operational losses on personal income returns if they don’t turn a profit, but won’t be able to grow internationally or beyond the 100-person natural shareholder limit. (To differentiate themselves from S Corps, Corporations are sometimes referred to as C Corps.)

Comparison Table: Business Organizational Structures

Choosing the Right Business Structure

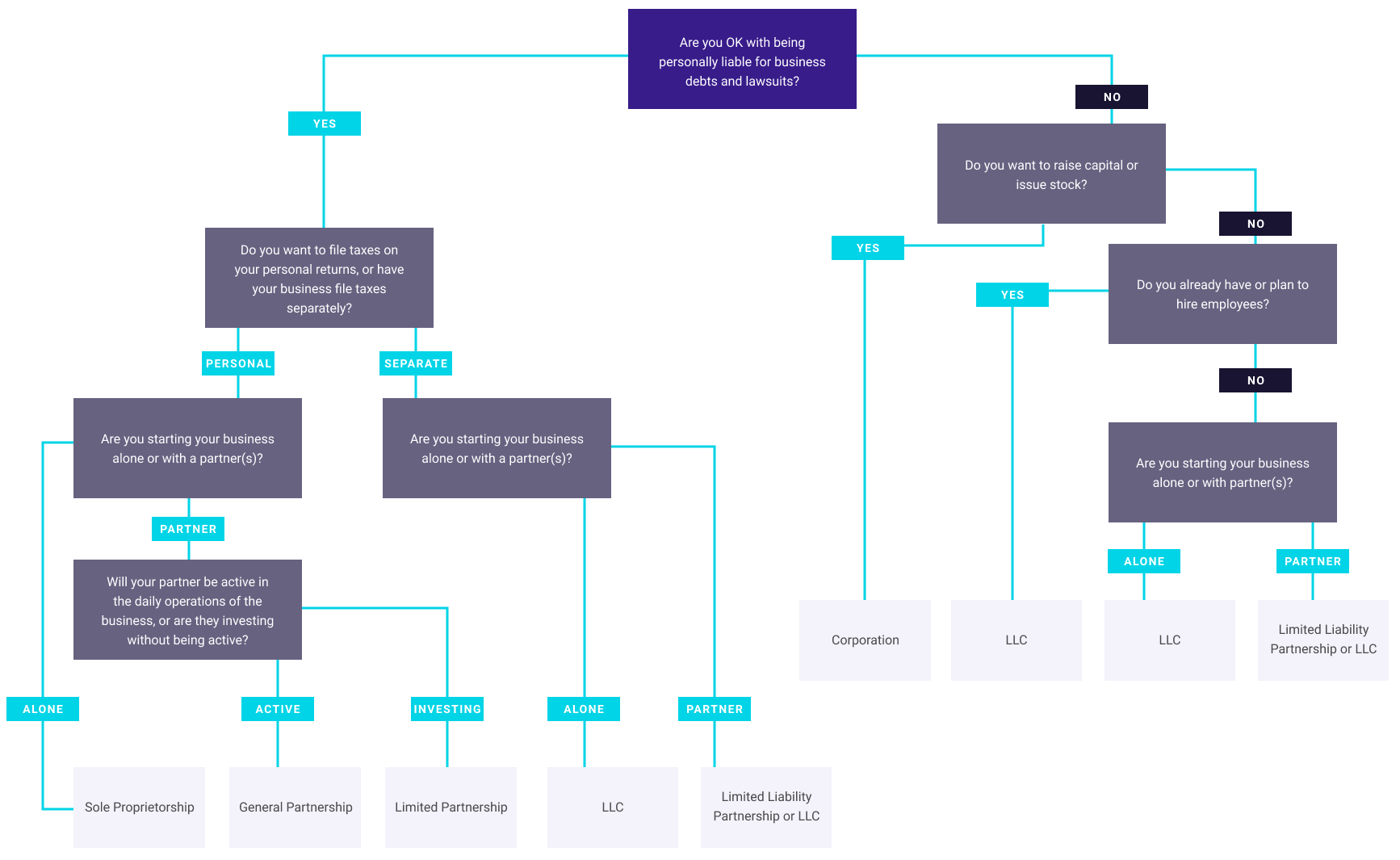

With a basic understanding of the different types of business structures, you can now decide which business structure is right for your ecommerce business. Choosing the best business structure for your particular situation will require you to think strategically about several core concepts.

Decide your level of personal liability

Owning a business comes with responsibility—also called liability. Liability comes in several forms, but the most important are legal liability and financial liability. When it comes to creating an online business, legal liability refers to the degree to which you’re personally liable for lawsuits filed against your company. Financial liability is the degree to which you’re personally liable for the finances of your business—whether or not creditors can come for your personal assets if your business owes money.

Business structures vary in terms of the amount of liability faced by their owners. Some business structures leave you personally liable for all debts, lawsuits, and other forms of liability associated with the business, while others provide you and your personal finances with a great degree of insulation from your business finances. Complex business structures like LLCs and Limited Partnerships tend to offer a greater degree of separation between the business and its owner. Simpler business structures like Sole Proprietorships and General Partnerships tend to have greater personal liability.

> Rule of Thumb: The simpler the business structure, the greater the level of personal liability.

Most ecommerce businesses don’t need the additional liability protection associated with more complex business models. Online merchants tend to use pre-packaged services instead of signing contracts with service providers, so their legal exposure is less than a business that’s entering into custom legal agreements with other companies. As long as your ecommerce business isn’t engaging in false advertising or selling customers’ credit card numbers, your chances of being sued are very low.

Sole proprietorships and general partnerships are great for starting an ecommerce business. As your company grows, you may want to consider forming an LLC or other, more formal business structure to provide you with greater liability protection and tax benefits.

Pick how you want to be taxed

Here’s where a little number crunching can go a long way. Personal taxes, self-employment taxes, and corporate taxes are all assessed at different rates. Though a percentage or two here and there might not seem like a big deal starting out, the more profitable your online store becomes, the more important your tax rate becomes. Before you know it, a 5% change could mean you owe thousands of dollars more from one year to the next.

Your ideal tax structure will depend on the type of business you’re starting, but here’s a good rule of thumb for online merchants: if you’re a small business, pass-through taxation (such as with a Sole Proprietorship or General Partnership) will make your taxes much easier to complete, and you’ll likely pay a lower rate than if you were taxed using the corporate model. If your business is more complex or has employees, you may be required to form an LLC or corporation.

> Rule of Thumb: If you’re a small online business, a Sole Proprietorship or General Partnership will make doing your taxes much simpler.

Do you structure your online business to as a pass-through entity whose profits go directly to any owners and get filed on their individual returns, or do you want to be taxed as an S Corp at a flat rate in hopes of saving yourself employment tax on top of salary earnings? Speak with a CPA to help get a better idea of how much you’d owe under each business structure based on your earnings bracket.

Figure out store ownership and responsibilities

The more owners your online store has, the more complicated your management structure will be. Unless it’s just you running a tight ship, you’ll need to have legally-binding agreements in place that determine who can make decisions, how profits will be divided out, and what happens in the event of a catastrophe (like death, disability, or bankruptcy).

For instance, corporations need a board of directors before they can make any sweeping changes to the business, whereas LLCs usually take issues to a management team who all weigh in on decisions that impact the company. Partnerships need partnership agreements detailing how decisions will be made.

Plan for the long term

The initial paperwork and fees it takes to register as a business vary by type; however, those aren’t all you’ll need to think about over the long term. Each business type also has a specific set of renewal obligations that can, and do, change from year to year, including deadlines to be met and fees to be paid. Skipping any of them can result in some high-stress complications.

The type of business structure you select for your online store also depends on how fast you’re looking to grow and who you plan on asking to help you generate operating capital. In some cases, a corporation fits the bill. For other brands, getting off the ground and making changes to the business type later is the biggest priority, pushing a Sole Proprietorship or LLC to the front of the line.

You’ll need to balance the advantages and disadvantages of each business model against your own business needs to choose which is best. Make sure that you’re planning ahead for a minimum of five years—you can always change your business model later if necessary, but it’s not something you’ll want to do often (since it tends to be time-consuming and expensive).

Flowchart: Business Structure Decision-Making

Create your business!

There’s no one “right” way to run a business, but choosing the right legal structure will help your business remain viable during its vulnerable first few years. Use the aforementioned resources to make sure that you’ve chosen the best business structure for your startup. If you’re looking to start your own online store, try Volusion’s all-in-one ecommerce platform. Built from the ground up for small ecommerce businesses, Volusion merchants sell an average of 2.8x more than merchants on other platforms.

from Volusion Ecommerce Blog | SMB Marketing, Design, & Strategy https://ift.tt/2XY3l8f via IFTTT

from Volusion Ecommerce Blog | SMB Marketing, Design, & Strategy https://ift.tt/2XY3l8f via IFTTT

No comments:

Post a Comment