If Pogo had its way, you’d get paid every time you stroll down Market Street in San Francisco. Or check your e-mail. Or open its app. The only catch is that you give your personal data to the consumer-focused fintech in return.

“We can almost create Honey for the real world,” said Pogo co-founder and chief executive Dom Wong, who is building the company alongside founders Oskar Melking and Shikhar Mohan. The startup seeks to use a few tech trends to its advantage. First, as data privacy becomes more of a concern, users are able to choose whether or not to share their information with companies. Pogo’s argument is that if they do share – why not get a benefit out of it?

Second, Pogo is a play on the rise of ecommerce tools such as Rakuten and Honey, browser extensions that automatically find cash, coupons and deals in return for your shopping history. And third, it is using a slew of APIs to plug into everywhere consumers exist, from their inbox, to their transaction history to, if they so choose, their location data.

To scale data in exchange for cash, the startup raised $14.8 million in venture capital in the form of a $12.3 million seed round led by Josh Buckley and a previously unannounced $2.5 million pre-seed round. Other investors in the startup include Slow Ventures, Village Global, Harry Stebbing’s 20VC, MrBeast’s Night Ventures, Hyper, Shrug, and creators including The Chainsmokers, Sophia Amoruso, Ryan Tedder and Lenny Rachitsky. Additionally the startup has money from the founders of Front, Rent the Runway, and, quite fittingly, Honey.

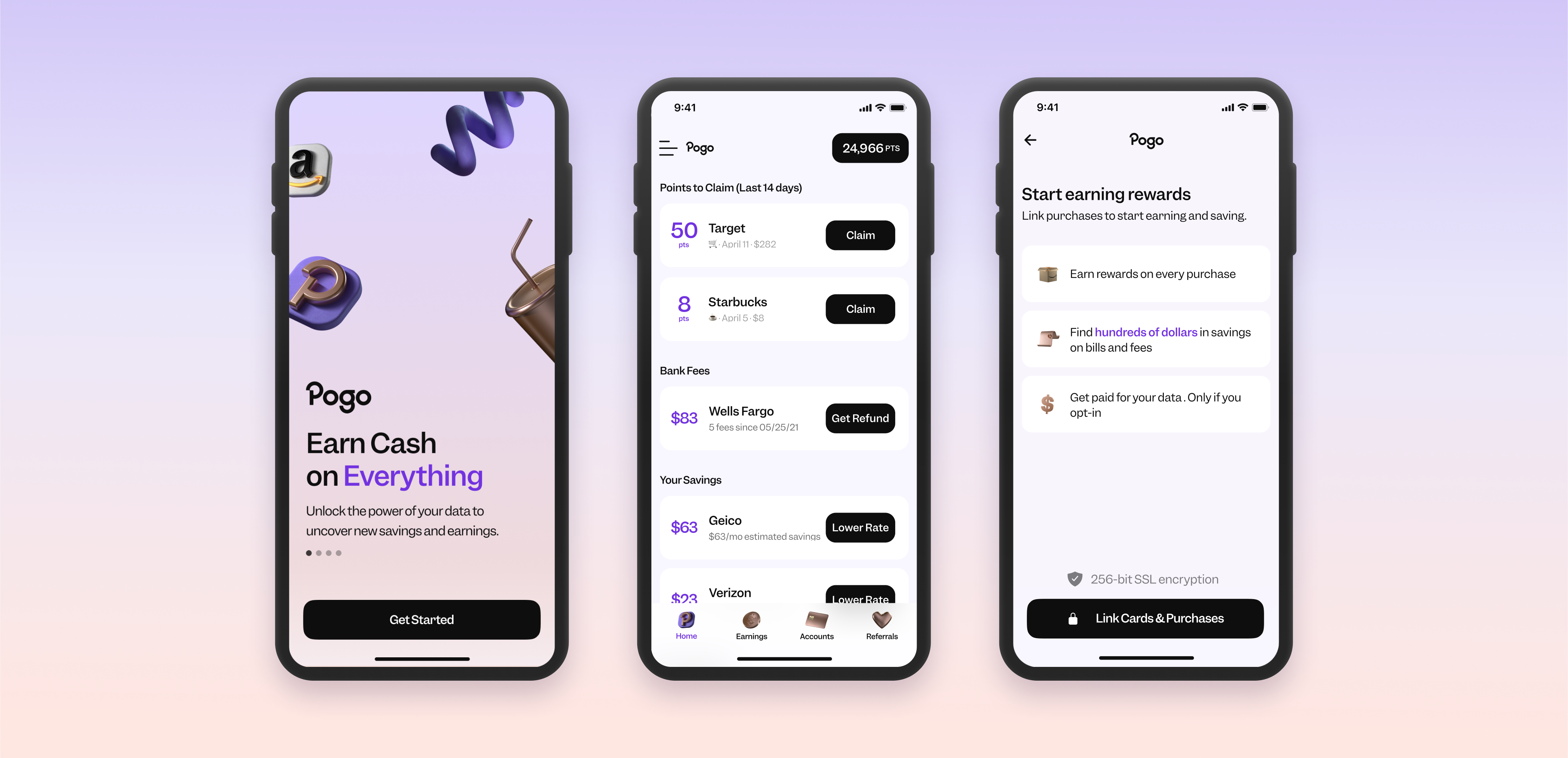

Here’s how it works: when a user joins the app, they are invited to send their data to the company. Once Pogo is connected with different sources of information, it begins to show rewards for purchases, or recommendations to “act on ” to save money.

Part of the app is helping people, who opt in, get paid for their data: “Pogo makes it easy for you to aggregate your data in one place, giving you the controls to get paid for use cases that you’re comfortable with, whether that’s anonymous market research or personalized marketing from trusted brands.” The other part of the app is similar to Honey, in that it works as a type of financial agent that sees your spending and makes suggestions, both for better deals or promotions you may not know about.

This isn’t entirely unheard of. Dosh, for example, is a venture-backed startup that makes deals with retailers, brands and payment providers, and then offers cash back to users once they purchase a product associated with connected providers. The startup was valued at $400 million in 2019, per TechCrunch reporting. There’s also Nigeria’s ThankUCash, which landed $5.3 million to set up cashback infrastructure, and existing work from PayPal, which launched a new credit card that offers 3% cashback on all PayPal purchases.

Image Credits: Pogo

It makes sense that there is activity here. As advertising dollars flock away from Facebook and Google, retailers and brands want to find new ways to reach potential customers. I think of it like this: you can choose to sell your new workout gear while you’re browsing Twitter, or in the locker room at your local Crunch gym. The latter finds a consumer when they’re more attuned to fitness and style, while the former bets that someone may just happen to be in the mood for a new set while surfing tech news.

Pogo doesn’t have exclusive partnerships with local businesses to have certain cashback feels in exchange for lead generation, a route that some neobanks have gone down. Instead, the startup just brings together all existing deals in one place – and it’s that interoperability between different data sources that Wong thinks is the biggest competitive advantage.

Pogo’s true differentiation is the invisible layer it provides for users just existing in the world that can turn notifications into money. A majority of Pogo’s users link location data because they get rewards while existing in the real world. “You’re walking by Wendy’s and a notification pops up for a free breakfast sandwich if you purchase it on the app. All you have to do is view it, and then you get paid and we get paid as well.”

Right now, the company gets largely paid through affiliate fees and exchange of data.

- opts in for a suggested insurance plan

- Clicks into a location-based offer

- Answers market research or campaign measurement questions

- Or scans Pogo card for a discount when buying a prescription

In the next iteration, Wong says, Pogo will suggest users to turn to fee-free banking alternatives, and then Pogo can make money through affiliate fees.

“We also think about how we can help you leverage offers that are at your fingertips today without formally brokering partnerships. This may mean surfacing publicly available content, or in the future, even personalized promotions in your inbox in a private, secure manner,” he wrote in an email. “For instance, imagine Pogo alerting you of the 40% off any item storewide coupon sitting unopened in your inbox next time you walk into a CVS.”

While Pogo certainly sees itself as an incentive aligned with customers, in order for it to make money, it needs to prove to other companies that personal data is a commodity. Pogo is going to have an intimate window into someone’s life, from where they live to their favorite coffee shop to just how many subscriptions they own. It’s similar to what a bank would see, but it’s a venture-backed startup that it wants you to trust.

The Electronic Frontier Foundation, a nonprofit that has defended civil liberties in the digital world since 1990, describes the idea of exchanging data for money as “data dividends.” In an essay, the organization urges consumers to rethink if getting money for their data really fixes the existent imbalance between users and corporations. The EFF asks a series of questions such as, who will determine what the cost of certain data is, and what makes your data valuable to companies? Plus, what does the average person gain from a data dividend, and what do they lose in exchange for that extra cash?

“EFF strongly opposes data dividends and policies that lay the groundwork for people to think of the monetary value of their data rather than view it as a fundamental right,” the organization wrote in a post. “You wouldn’t place a price tag on your freedom to speak. We shouldn’t place one in our privacy, either.”

Over e-mail, Wong said that there are existing market rates for common data fees, but the startup is working on a pricing strategy based on “a lot of greenfield territory that simply isn’t possible today.”

“For instance, our ability to serve a location based offer or ad that also takes into account your past purchases allows us to command rates that are many orders of magnitude higher than your typical ad placement,” he continued. “Another example would be the ability for brands to get real-time consumer feedback based on verified purchases. The ability to do so is incredibly slow and clunky today, and it’s not unusual for brands to pay hundreds of dollars per response based on rates set by existing behemoths that do billions of dollars a year in revenue.”

Wong isn’t too worried about losing user trust, just yet. So far, the app has been used by “hundreds of thousands of families” and the startup claims it has generated millions of dollars in savings and earnings.“We’re being very intentional about how we think about partnerships here, which is why we want to continue segmenting anonymized market research versus personalized targeting based on your Instagram feed.”

from TechCrunch https://ift.tt/SoqcGar via IFTTT

from TechCrunch https://ift.tt/SoqcGar via IFTTT

No comments:

Post a Comment